The higher hydroelectric contribution would mainly explain the drop in the central system. In the north, which mainly supplies industrials, there is a lower supply in relation to the expected demand for 2015.

Marginal energy costs would decrease in SIC, but could increase in SING

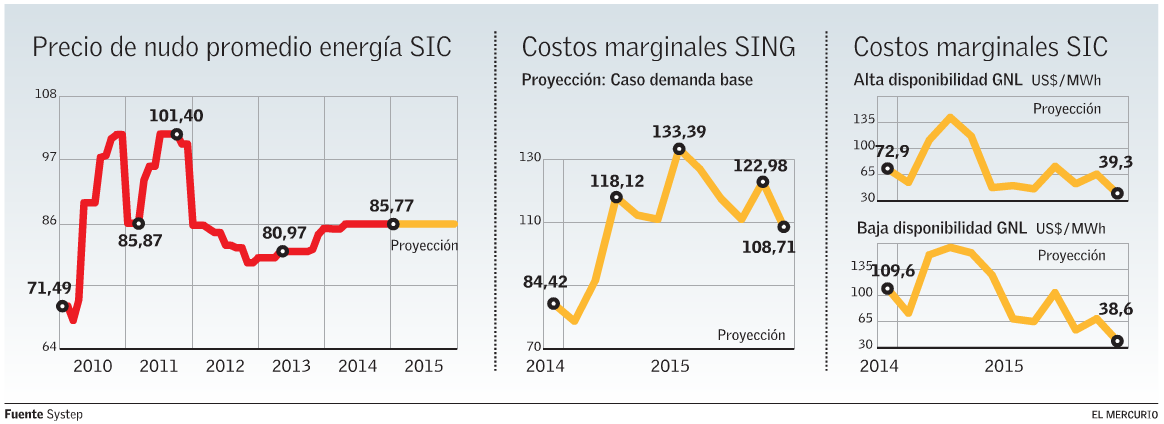

A different scenario could be faced in 2015 by large industrial energy consumers or free customers whose consumption is governed by marginal cost levels, meaning the average price of the energy generated by the most expensive power plant entering the system, and which marks transactions in the spot market.

The government set as one of its main goals to reduce these costs by 30% by the end of Michelle Bachelet’s administration. That is, the 2013 average of US$ 151.36 per MWh was lower than US$ 105.96 per MWh in 2017.

According to Systep’s data, marginal costs in the Norte Grande Interconnected System (SING) would increase from an average price of US$ 84 per MWh in December of this year to US$ 109 per MWh in November 2015, considering an average demand. As can be seen, although they foresee an increase in costs, they are still very close to the government’s objectives. According to the consultant, in the SING, the marginal cost reflects the balance between demand and supply, and as can be seen, the base energy capacity is not entering at the same rate as demand. Even so, Systep warns that it would not be strange for demand to grow less than expected due to the deceleration of many activities in the area, such as mining. In this case, marginal costs could reach US$ 90 per MWh. In the SING, most of the energy sources are thermal.

In the Central Interconnected System (SIC), meanwhile, the firm estimates a considerable drop in marginal costs, both in a scenario of low and high availability of Liquefied Natural Gas (LNG). In the first case, they project a drop from US$ 73 per MWh to US$ 39 per MWh, while in the second case they foresee a reduction from US$ 110 per MWh to US$ 39 per MWh. In both scenarios, an average hydrology is considered, i.e., higher than that of the last year. The difference with the SING is explained by the hydroelectric plants.

Price to regulated

According to Systep’s projections, next year, the average price of energy for regulated customers -residential or commercial- will not experience major changes and will remain at levels close to US$ 86 per MWh. This, without considering the indexations made every year in April and October by the National Energy Commission (CNE).

The consulting firm explains that this projection responds to the fact that there are no new contracts coming into effect in 2015. On the other hand, contracts for block 1 awarded in the last tender will be incorporated into the price only in early 2016, although they warn that these are small volumes in relation to the energy currently contracted.

In the recent supply tender, contracts were awarded at an average price of US$ 107 per MWh, well below the US$ 130 per MWh of more than a year ago. The process had four blocks, and number one – to which Systep refers – considers a volume of 1,000 GWh per year for a period of 15 years, and is composed of three hourly blocks.